The classical Markowitz’s mean-variance portfolio formulation ignores heavy tails and skewness. High-order portfolios use higher order moments to better characterize the return distribution. Different formulations and fast algorithms are proposed for high-order portfolios based on the mean, variance, skewness, and kurtosis. The package is based on the papers Zhou and Palomar (2021) and Wang, Zhou, Ying, and Palomar (2022).

The package can be installed from CRAN or GitHub:

# install stable version from CRAN

install.packages("highOrderPortfolios")

# install development version from GitHub

devtools::install_github("dppalomar/highOrderPortfolios")To get help:

library(highOrderPortfolios)

help(package = "highOrderPortfolios")

?design_MVSK_portfolio_via_sample_moments

?design_MVSK_portfolio_via_skew_tTo cite highOrderPortfolios in publications:

citation("highOrderPortfolios")library(highOrderPortfolios)

data(X50)

# non-parametric case: estimate sample moments

X_moments <- estimate_sample_moments(X50)

# parametric case: estimate the multivariate skew t distribution

X_skew_t_params <- estimate_skew_t(X50)

# choose hyper-parameter moment weights for the MVSK formulation

xi <- 10

lmd <- c(1, xi/2, xi*(xi+1)/6, xi*(xi+1)*(xi+2)/24)

# design portfolio

sol_nonparam <- design_MVSK_portfolio_via_sample_moments(lmd, X_moments)

sol_param <- design_MVSK_portfolio_via_skew_t(lmd, X_skew_t_params)

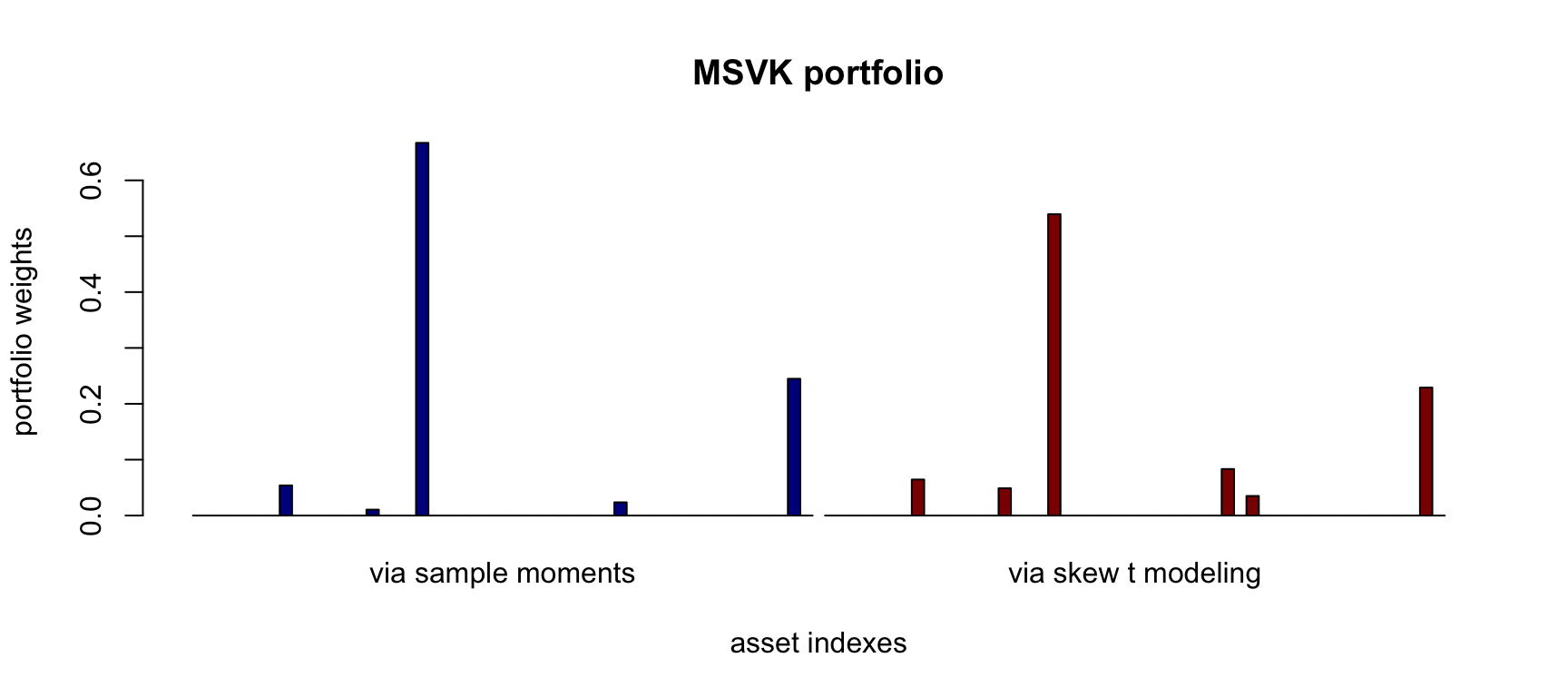

# plot

barplot(cbind("via sample moments" = sol_nonparam$w, "via skew t modeling" = sol_param$w), beside = TRUE,

col = c(rep("darkblue", 50), rep("darkred", 50)),

main = "MSVK portfolio", xlab = "asset indexes", ylab = "portfolio weights")

For more detailed information, please check the vignette: CRAN-vignette and GitHub-vignette.

README file: CRAN-readme and GitHub-readme.

Vignette: CRAN-vignette and GitHub-vignette.